Nobody wants to pay more taxes than they must. For self-employed business owners, who pay both sides of employment taxes, this is especially true.

Let’s see if the following strategy can help you hang onto more of the dollars you make. We’ll meet Dr. Abe Erskine who feels he is paying too much in taxes and that he started too late on his retirement savings.

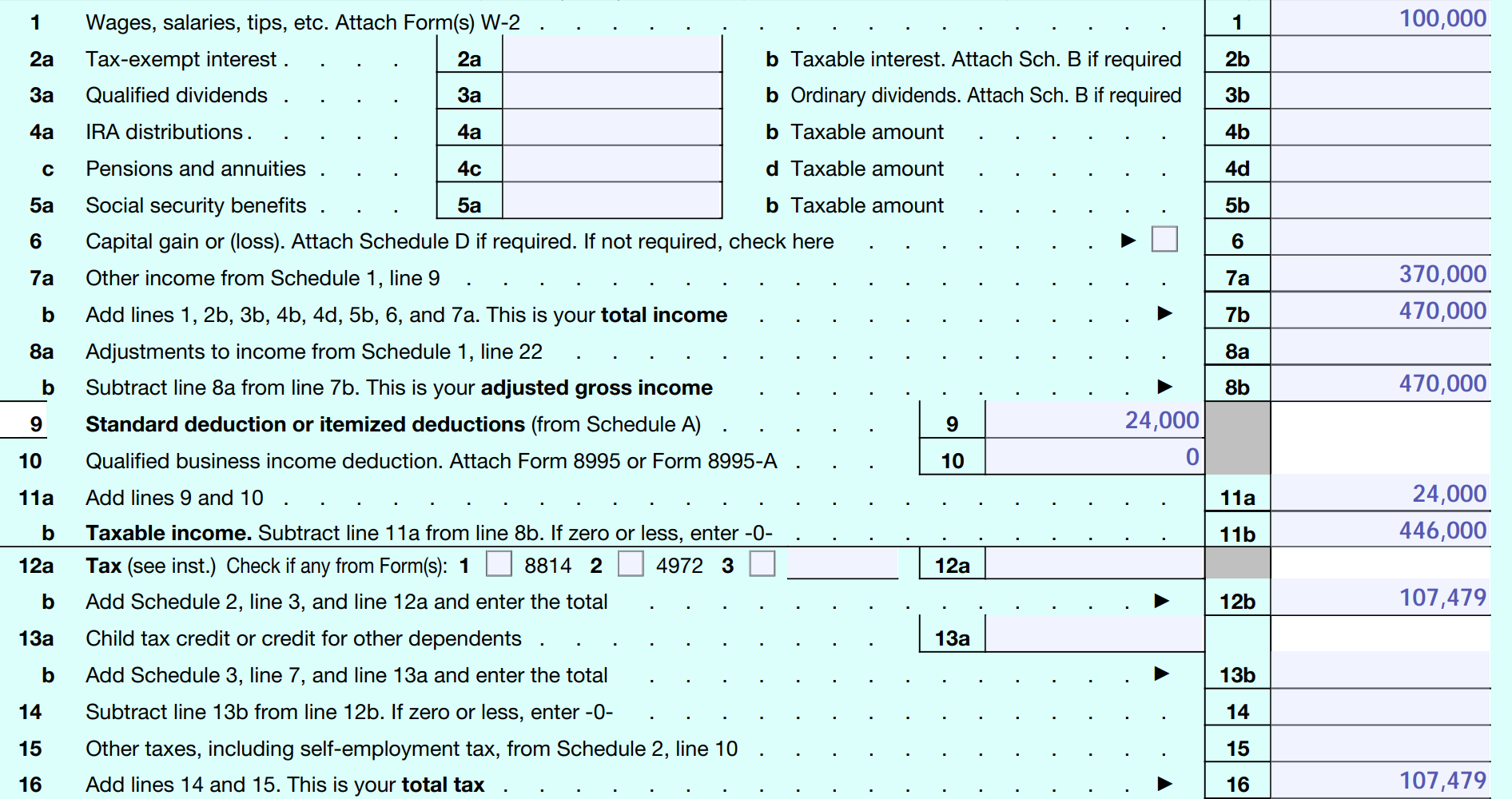

$107,479! That's what I paid in taxes last year. I need help with that.

I'm not sure I'll have enough to retire the way I want.

Like most business owners, Dr. Erskine invested in his family first, his business second, and his retirement third, or not at all. Only as he neared 60 years of age did he notice that he was not on the path to the golden years he dreamed of.

Practice Name: Vita-Ray Health

Entity Type: LLC filing as a S-Corporation

Employees: 5

Employee Payroll: $200,000

Business’ Fair Market Value: $1,500,000

Income after Business Expenses: $500,000

Taxes Paid Last Year: $107,479

Age: 58

Filing Status: Married Filing Jointly

Retirement Savings: $500,000

Annual Retirement Contribution: $30,000

Desired Monthly Retirement Income at 67: $20,000

Estimated Monthly Retirement Income at 67: $13,266.90

Estimated Monthly Shortfall in Retirement: $6,733.10

Clearly, Dr. Erskine needed help in accomplishing his goals of reducing his taxes and increasing his retirement savings. So, we went to work and put together a Design Team focused on his success.

Let’s look at how this Design Team assisted him on his taxes.

BEFORE

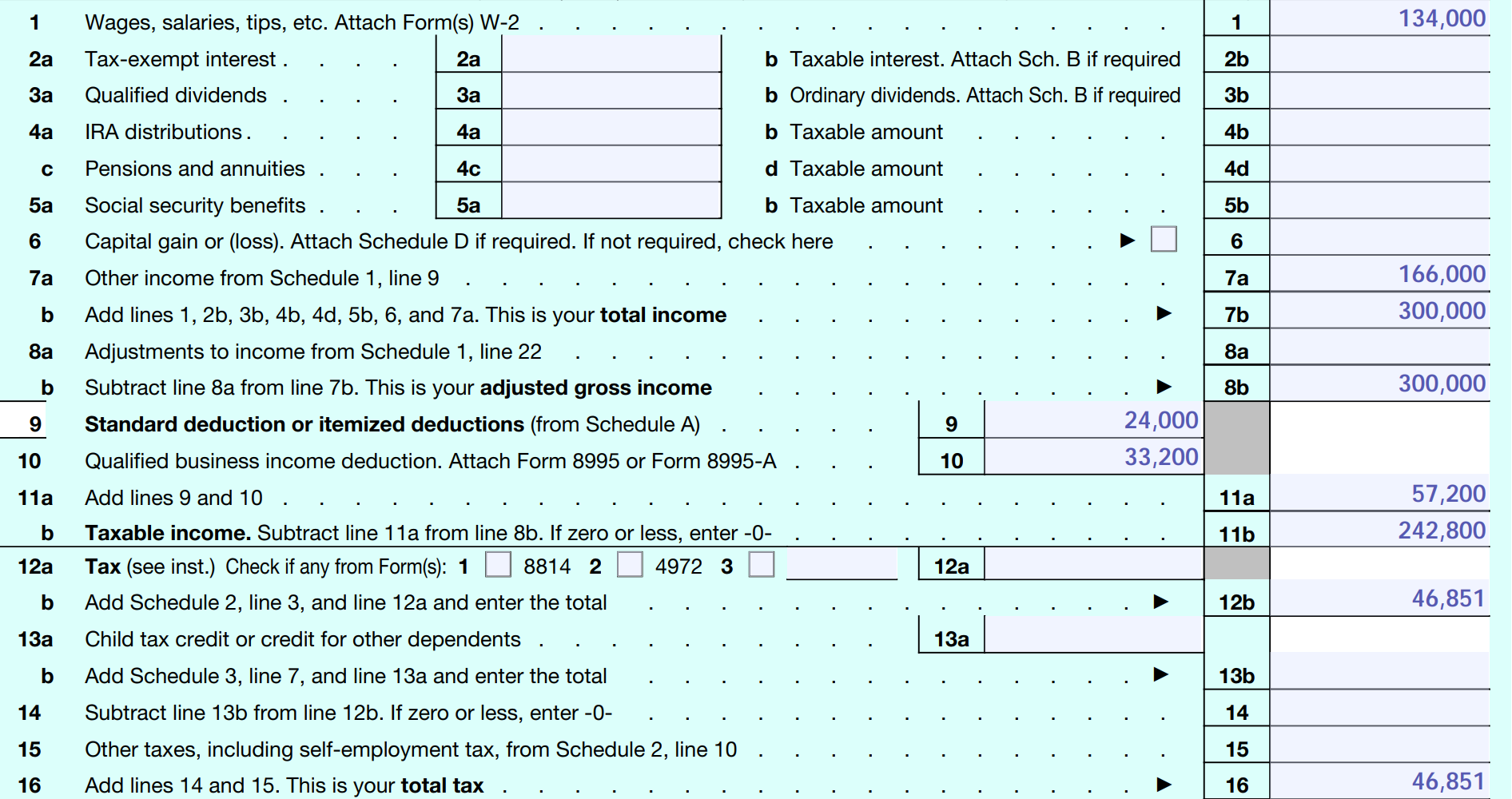

AFTER

IMPACT

How did his Team manage to provide Dr. Erskine over $60,000 in tax savings? The answer is in the Advanced Retirement Plan Design Strategy that was built with his goals in mind.

Cross-Tested 401(k) Plan

Cash Balance Pension Plan

“Combo”

Plan

Before his Design Team assisted him, Dr. Erskine only had a SEP IRA for his retirement plan. After getting expert help though, he switched over to a combination retirement plan comprised of a Cross-Tested 401(k) Plan + Cash Balance Pension Plan. This change is what allowed Dr. Erskine to lower his taxes by over $60,000 and to help super charge his retirement savings to $200,000. Let’s look at a comparison of these plan designs.

No Data Found

The big takeaways here are on taxes and cost. We see above how Dr. Erskine increased his contributions from $30,000 to $200,000 for himself, but let’s look at the cost involved. To fund his SEP IRA for himself at $30,000, Dr. Erskine incurred costs of $21,640. To fund his Combo Plan, Dr. Erskine will have to pay $31,000. That’s a significant increase, but when we look at the impact it makes, it’s no wonder Dr. Erskine was excited to do this. With the SEP IRA, 58% of each dollar going to the plan was his. Now, with his Combo Plan, 89% of each dollar going to the plan is his. While it might appear that this is detrimental to his employees, everyone is getting more dollars than they were before in this new plan design, as shown when you hover over anyone’s slice in the doughnut charts below.

SEP IRA – Employee’s Share of Retirement Benefits

Combo Plan – Employee’s Share of Retirement Benefits

Now that Dr. Erskine has knocked out his first goal of Reducing his Taxes, let’s see how his Design Team did with his second goal of Retirement Savings.

Retirement Savings:

$500,000

Business’ Fair Market Value: $1,500,000

Years Until Retirement: 9

Desired Monthly Income at 67: $20,000

BEFORE – SEP IRA

Annual Retirement Contribution: $30,000

Estimated Monthly Retirement Income at 67: $13,266.90

Estimated Monthly Shortfall in Retirement: $6,733.10

AFTER – COMBO PLAN

Annual Retirement Contribution: $200,000

Estimated Monthly Retirement Income at 67: $20,054.42

Estimated Monthly Shortfall in Retirement: $0

We can see that with the SEP IRA alone, Dr. Erskine would have fallen significantly short of his retirement goal. However, with the help of his Design Team and an Advanced Retirement Plan Design Strategy built with his goals in mind, he was able to greatly accelerate his qualified savings amount and meet his retirement goal with the use of his very own Combo Plan!

Dr. Erskine had 2 goals when he reached out, Reduce Taxes and increase Retirement Savings.

Now, it’s your turn! See if a Combo Plan would be a fit for your business. Reach out to us below!

Case studies may not be representative of all clients and are not indicative of future performance or success.

Lorio Wealth Management does not provide tax, accounting, or legal advice. Any tax statements contained herein were not intended or written to be used to avoid U.S. federal, state, or local tax penalties. Clients should contact their own independent advisors as to any tax, accounting, or legal considerations when determining if these statements may be beneficial to their specific circumstances.

FORM 1040 Line 8b – Adjusted Gross Income

The Tax Cuts and Jobs Act gives business owners the opportunity to unlock a powerful, new tax deduction for pass through businesses. The Section 199A Deduction says that eligible taxpayers may be entitled to a deduction of up to 20 percent of qualified business income (QBI) from a domestic business operated as a sole proprietorship or through a partnership, S corporation, trust or estate.

FORM 1040 Line 10 – Qualified Business Income Deduction

However, for taxpayers with taxable income that exceeds $321,600 for a married couple filing a joint return, or $163,300 for all other taxpayers, the Section 199A deduction is subject to limitations such as the type of trade or business, the taxpayer’s taxable income, the amount of W-2 wages paid by the qualified trade or business and the unadjusted basis immediately after acquisition (UBIA) of qualified property held by the trade or business.

More particulars may be found here: https://www.irs.gov/newsroom/tax-cuts-and-jobs-act-provision-11011-section-199a-qualified-business-income-deduction-faqs.

| Name | Age | Wage | SEP IRA | % of Benefit |

|---|---|---|---|---|

| Dr. Feel Good | 58 | $280,000 | $30,000 | 58% |

| Cat | 45 | $50,000 | $5,350 | 10% |

| Ana | 40 | $45,000 | $4,815 | 9% |

| Ron | 35 | $40,000 | $4,280 | 8% |

| Eva | 30 | $35,000 | $3,745 | 7% |

| Sam | 25 | $30,000 | $3,210 | 6% |

| Name | Age | Wage | 401(k) + Cash Balance | % of Benefit |

|---|---|---|---|---|

| Dr. Feel Good | 58 | $280,000 | $200,000 | 89% |

| Cat | 45 | $50,000 | $6,200 | 3% |

| Ana | 40 | $45,000 | $5,650 | 3% |

| Ron | 35 | $40,000 | $5,100 | 2% |

| Eva | 30 | $35,000 | $4,550 | 2% |

| Sam | 25 | $30,000 | $4,000 | 2% |

In determining Dr. Abe Erskine’s Retirement Savings, the below Future Value calculation was used to determine the impact of his “BEFORE – SEP IRA” and “AFTER – Combo Plan” results.

Before – SEP IRA

After – Combo Plan

Present Value

Interest

Payment

# of Years

Future Value Result

$500,000

7%

$30,000

9

$1,278,569.27

Present Value

Interest

Payment

# of Years

Future Value Result

$500,000

7%

$200,000

9

$3,314,827.36

In each case, these were added to his Business’s Fair Market Value of $1,500,000. For simplicty, this figure is the value of his business at the time of Dr. Erskine’s retirement. Then, a 4% withdrawal rate was applied. This result was supplemented by his age 67 Social Security Estimates from the Social Security Quick Calc resource. The results of these calculations are shown in the Retirement Savings section above.

Tracking #1-05025756